Is Aviation Better in Europe or the U.S. in 2025? The Full Industry Breakdown

The aviation industries in Europe and the United States are both poised for significant developments in 2025, each presenting unique opportunities and challenges. This article delves into key aspects such as market size, growth projections, environmental initiatives, and operational costs to provide a comprehensive comparison.

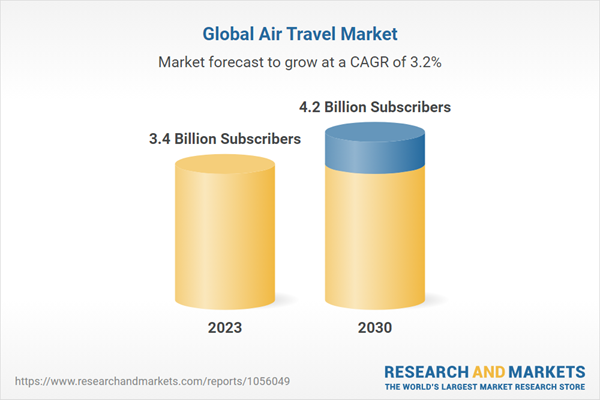

Market Size and Growth Projections

In 2025, the U.S. aviation market is expected to reach a valuation of approximately USD 86.72 billion, with projections indicating growth to USD 105.00 billion by 2030, reflecting a compound annual growth rate (CAGR) of 3.90% . Conversely, Europe’s aviation market is projected to be valued at USD 62.49 billion in 2025, with an anticipated increase to USD 77.36 billion by 2030, corresponding to a CAGR of 4.36% . While the U.S. market is larger in absolute terms, Europe’s slightly higher growth rate suggests a dynamic expansion trajectory.

Passenger Traffic and Capacity

The global aviation industry is on track to transport 5.2 billion passengers in 2025, marking a 6.7% increase compared to 2024 . In Europe, seat capacity for the first quarter of 2025 is projected at 101.5% of 2019 levels, indicating a robust recovery and potential surpassing of pre-pandemic figures . In the U.S., capacity growth is more modest, with a 1.1% year-over-year increase expected in the first quarter of 2025, totaling 270 million available seats .

Environmental Initiatives

Europe is taking significant steps toward environmental sustainability in aviation. The RefuelEU Aviation Regulation, approved in 2023, mandates that Sustainable Aviation Fuels (SAF) comprise 2% of fuel at European airports by 2025, with a gradual increase to 70% by 2050 . This initiative underscores Europe’s commitment to reducing aviation’s carbon footprint. In contrast, the U.S. has yet to implement comparable federal mandates, though individual airlines are exploring sustainable practices.

Operational Costs and Pricing

Operational costs, particularly labor expenses, significantly impact airline ticket pricing. U.S. airlines face labor costs that are 47% higher than those of their European counterparts, contributing to elevated ticket prices . European carriers benefit from a competitive landscape with numerous low-cost options, enabling them to maintain more affordable fares despite operational expenses.

Trade Policies and Industry Impact

Recent U.S. tariffs on European imports, including a 20% levy on EU goods, have introduced complexities into the aviation sector . These tariffs affect aircraft, engines, and components, potentially increasing costs for manufacturers and airlines, and may influence fare prices and operational efficiency.

Conclusion

Both Europe and the United States exhibit robust aviation markets with distinct characteristics. Europe’s proactive environmental policies and competitive pricing contrast with the U.S.’s larger market size and higher operational costs. Trade policies further differentiate the two regions, adding layers of complexity to their respective aviation landscapes.

Comments